Employer FAQ

EMPLOYER FREQUENTLY ASKED QUESTIONS

Membership

- What employees are covered by MFPRSI?

Full-time firefighters and police officers employed by one of the 49 participating cities in the Iowa Code Chapter 411 (“Chapter 411”) retirement system. - Can an employee opt out of MFPRSI?

A fire chief or a police chief, who will not complete 22 years of service under MFPRSI by the time they reach age 55 can submit a written request for exemption from MFPRSI. City should read Iowa Code Section 384.6(1)(b) concerning city contributions.

Contributions

- How much does the employee contribute to MFPRSI?

Each active member contributes a fixed percent of his or her earnable compensation. Presently, the member’s contribution rate is 9.675%. - How much does the city contribute to MFPRSI?

The city contribution rate is actuarially adjusted each year with a statutory minimum of 17%. MFPRSI announces the new city rate to be effective July 1st by the end of the prior calendar year. Click here for more information on contribution rates. - What is earnable compensation?

Earnable compensation is the annual salary a member earns for services rendered as a firefighter or police officer with a participating city employer. However, earnable compensation excludes overtime compensation, meal and travel expenses, uniform allowances, severance pay, mandatory deferred compensation, and any lump-sum payments at termination for accumulated sick and vacation leave. Click here for more information on MFPRSI Administrative Rule 3.1(4). - How are contributions submitted to MFPRSI?

Contributions are submitted to MFPRSI via ACH. The city can initiate the ACH with their financial institution or submit the ACH through MFPRSI’s employer portal (https://employer.mfprsi.org/). - When are contributions due?

Contributions are due by the 15th of the month following the month collected. - How are employee earnable compensation and contributions reported to MFPRSI?

Detail contribution reports are submitted to MFPRSI on a quarterly basis through MFPRSI’s employer portal (https://employer.mfprsi.org/). See https://www.mfprsi.org/employers/compensation-reporting/ for report formatting.

Benefits

- What types of benefits does MFPRSI offer?

MFPRSI offers several types of benefits, including the following:

• Service

• Deferred Retirement Option Plan (DROP)

• Terminated vested

• Disability

• Death - What are the eligibility requirements of a service retirement?

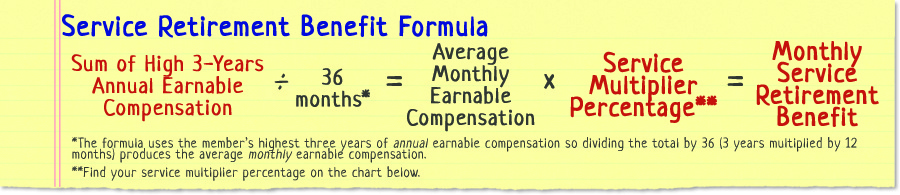

To receive a basic service retirement, a member must be vested and at least 55 years old. - What is the basic service retirement?

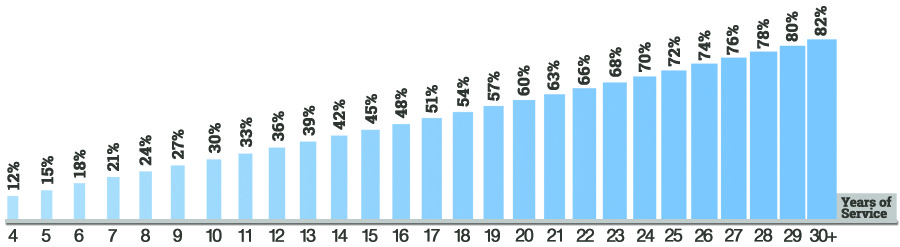

With 22 years of service the basic service retirement is equal to 66% of a member’s average final compensation. For each year of service beyond 22, a member can add an additional 2% credit. Please refer to the Basic Benefit Multipliers chart below. - How is the average final compensation determined?

The average final compensation is the average of a member’s earnable compensation using their highest 3 years of compensation.

To find the basic benefit multiplier percentage, locate the number of years served on the chart. The corresponding percentage is the multiplier percentage used in the calculation above.

DROP

- What is DROP?

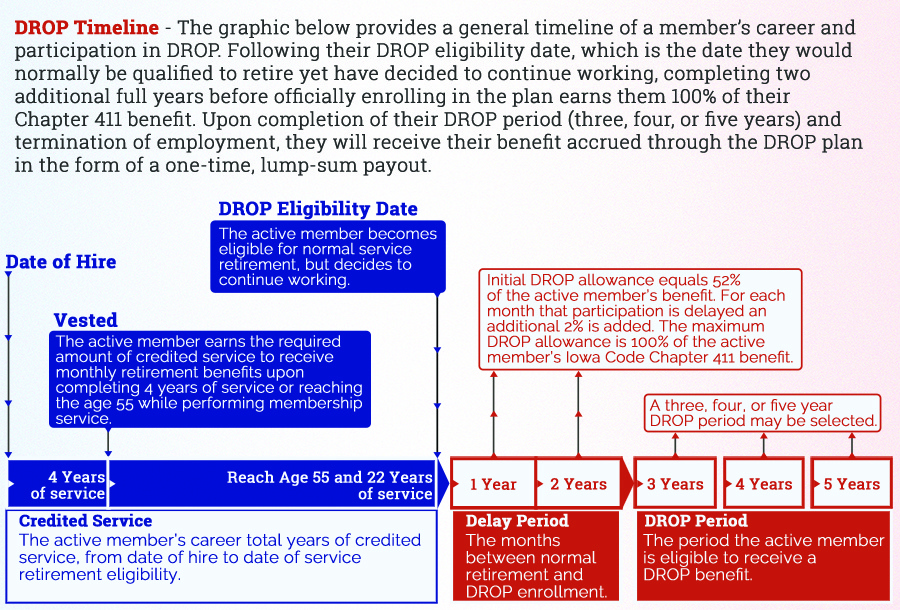

Deferred Retirement Option Plan (DROP) is a distribution option available to active members. - Who is eligible for DROP?

Active members, at least 55 years old, and have 22 or more years of service, are eligible for DROP. - How does DROP work?

If a member has reached eligibility for a normal service retirement but decided to continue working they may enroll in DROP. Once enrolled, MFPRSI will establish an account in which a portion of their benefit, called the “Chapter 411 Benefit” for purposes of DROP, will be credited. - What comprises the Chapter 411 Benefit?

The Chapter 411 Benefit will be calculated using the following steps:

• A minimum percentage of 52% multiplied against the Chapter 411 Benefit, plus,

• An adjustment percentage determined by the number of months between the date the member elects to participate in DROP and the date the member was initially eligible to participate multiplied against the Chapter 411 Benefit. - How much does the DROP benefit increase for each month delayed?

For each month a member delays participation an additional 2% is added to the adjustment percentage. Therefore, if a member delays the full 24 months, they will get 48% as their adjustment percentage (24 months x 2%). Add that to the minimum 52% and their total DROP benefit would be 100%. - What is the maximum DROP percentage?

The maximum DROP percentage is 100%. - How long can a member participate in DROP?

A member may elect a participation period of 3, 4, or 5 years.

Terminated Benefits

- What does “terminated-vested” mean?

A member may qualify for terminated-vested status if they end their position as a firefighter or police officer with one of the 49 participating cities in the retirement system and fit one of the following criterion:

• If they have at least 4 years of service and are not yet age 55, or

• If they have less than 22 years of service and are older than age 55. - What are the benefits of being vested?

Becoming vested gives the member a permanent future right to a benefit with MFPRSI. Upon reaching age 55 the member is eligible for a monthly lifetime benefit. If they leave MFPRSI-covered employment as a vested member, they may leave their money in MFPRSI. - What are the terminated-vested benefits?

The amount of terminated-vested pension is a fraction of the pension they would have received if they had been eligible for a service retirement benefit at the time of their employment ending.

The fraction is 4/22 for four years of service. Each additional year beyond that is credited with an additional 1/22 up to 22 total years. For years of service over 22, additional credits may be earned. - Does a member forfeit their MFPRSI benefits if terminated by the city?

No, if the member is vested at termination, their pension rights cannot be taken away. It should be noted, however, that the annual readjustment of pensions (escalation) is available only to members who served at least 22 years and attained age 55 prior to termination of service. - What if the member is not vested at the time of termination?

Members who terminate service (vested or non-vested) may withdraw all their contributions from the date of hire, with interest calculated for the period of membership. The contributions withdrawn will be credited with an annualized simple interest rate determined by the Board of Trustees, currently set at 5%. If a member does withdraw contributions, they waive all claims for other benefits for the period of membership for which the withdrawal is made. Non-vested members should be directed to MFPRSI’s refund application available on MFPRSI’s website at https://www.mfprsi.org/printable-forms/.

Disability Benefits

- What are the eligibility requirements of a disability benefit?

The disabling injury or illness must be considered as lasting one year or longer, and the member must be considered a “member in good standing”. - What is a “member in good standing”?

A “member in good standing” means any member in service who has not been terminated by the employing city. Termination procedures initiated by the chief of police or chief of the fire department do not become final or adversely impact a member’s status as a member in good standing until all appeals provided by an applicable collective bargaining agreement or by law have been exhausted. Disciplinary action other than discharge does not adversely affect a member’s status as a member in good standing.

If a member is not a “member in good standing” after all appeals have been exhausted, disability benefits will terminate, and the member will be required to return all disability benefits received plus interest to MFPRSI. - What is the difference between an Accidental disability and an Ordinary disability?

The key difference between an accidental and an ordinary disability benefit is whether the injury or illness meets the definition of accidental under Iowa Code Chapter 411. If a member suffers an injury as the result of an injury or disease incurred in or aggravated by the actual performance of duties or arising out of or in the course of employment as defined by statute or are disabled due to a presumed illness, then the member is eligible to apply for an accidental disability benefit. An ordinary disability benefit, meanwhile, is provided if the injury or illness does not meet the definition of accidental. - What is the benefit calculation for an accidental disability?

The accidental disability benefit calculation is equal to 60% of the sum of the member’s average final compensation. The service retirement benefit formula may be substituted if it produces a higher benefit. - What is the benefit calculation for an ordinary disability?

If the member has more than 5 years of service, the ordinary disability benefit calculation is equal to 50% of the member’s average final compensation, but if the member has fewer than 5 years of service, the ordinary disability calculation is equal to 25% of the member’s average final compensation. The service retirement benefit formula may be substituted if it produces a higher benefit. - How does a member file for disability benefits?

The disability application is available on MFPRSI’s website at https://www.mfprsi.org/printable-forms/. The city must complete the employer sections of the application and provide incident reports related to the injury or disease. - Does MFPRSI pay temporary disability benefits?

No, MFPRSI does not pay temporary disability benefits; instead, temporary disability benefits are determined and paid for by the city. Cities should review Iowa Code Chapter 411.6(5)b. - Does MFPRSI pay medical costs for job related injuries and diseases?

No, MFPRSI does not pay medical costs; instead, medical cost benefits are determined and paid for by the city. Cities should review Iowa Code Chapter 411.15. - Does MFPRSI disability determination impact the city’s responsibility for medical costs?

No, medical cost benefits are determined and paid for by the city. Cities should review Iowa Code Chapter 411.15.

Death Benefits

- Does MFPRSI provide active death benefits?

Yes, MFPRSI provides both accidental and ordinary death benefits. - What is meant by “accidental death”?

An active member who dies from causes sustained in the line of duty. Heart, lung, respiratory tract disease, cancer, and certain infectious diseases are presumed to have been contracted in the line of duty and meet the eligibility requirements. - What is the accidental death benefit?

Surviving spouses, dependent children, or dependent parents are entitled to a pension equal to 50% of the sum of the average final compensation. Each dependent child is entitled to a pension equal to 6% of the average earnable compensation of the active membership as reported by the retirement system’s actuary.

In addition to the monthly accidental death benefit payment, spouses, children, or dependent parents may be entitled receive a single traumatic death lump sum payment of $100,000. - What is meant by “ordinary death”?

The death of an active member with at least 1 year of service and terminated-vested members whose death does not meet the definition of an accidental death. - What is the ordinary death benefit?

A beneficiary is entitled to a lump-sum equal to the greater of a return of contributions plus interest or 50% of the active member’s earnable compensation during the final year of service before his/her death.

Alternatively, surviving spouses or dependent children may elect one of the following:

• A pension equal to 40% of the sum of the member’s average final compensation (using up to the highest 3 years of compensation, if applicable), but not less than 20% of the average earnable compensation of MFPRSI’s active membership as reported by the actuary.

• Dependent children may receive a monthly pension equal to 6% of the average earnable compensation of the active membership as reported by our actuary. - When a retired member dies, is there a benefit payable to his/her surviving spouse and dependent children?

Yes, the surviving spouse and dependent children are eligible for a death after retirement benefit if the retired member who dies was receiving an annuity with survivor benefits, ordinary disability, or accidental disability retirement. - What is the benefit the surviving spouse and dependent children of a retired member will receive?

Surviving spouses are entitled to an amount equal to 50% of the member’s gross benefit, but not less than 20% of the average earnable compensation of the active membership of the retirement system as reported by the actuary.

If the member retired on a service retirement benefit and selected one of the optional forms of benefit instead of the basic benefit, the eligibility and benefits are paid in accordance with the option chosen.

Dependent children are entitled to a pension equal to 6% of the average earnable compensation of the active membership as reported by the actuary.